Top Hits from Lewandowski v. Johnson and Johnson Proposed Lawsuit

NOTE: This post originally appeared on TrueClaim's blog (opens in a new tab).

A proposed class action lawsuit (opens in a new tab) was filed against Johnson and Johnson on February 5, 2024. I read the whole 74-page proposed lawsuit and compiled the most interesting parts of the suit along with my thoughts and takeaways. The lawsuit offers a scathing review of the management of the prescription-drug benefits for JnJ employees, and, in doing so, a refreshingly clear explanation of the perverse incentives and potential corrective actions in the world of self-insured employer benefits. I’d highly recommend reading the “FACTUAL AND LEGAL BACKGROUND” section (pages 9-31) if you’re not up to speed on how this dysfunctional system operates in the U.S.

Lewandowski v. JnJ Top Hits

Defendants agreed to make Johnson and Johnson’s prescription-drug plans and their beneficiaries pay, on average, roughly 6 times as much as the PBM (or a PBM-owned pharmacy) paid for those very same drugs. Not incidentally, Johnson and Johnson is a leading drug maker that earns billions of dollars a month selling drugs. (Page 4)

Starting off strong, it’s objectively hilarious that the first major "breach of healthcare benefits fiduciary duty" case under ERISA is against Johnson and Johnson, a large drug manufacturer, and the lawyers know it.

Prudent fiduciaries would… (pretty much every page)

For all my benefits leaders reading, you can literally search this document for the term "Prudent fiduciaries" (both singular and plural) to find 20+ actionable steps towards being a good fiduciary for your prescription drug plan. It’s nice when the path towards prudence is made so clear!

If you don’t feel like CMD-F’ing your way through the 74 pages, click here (opens in a new tab) and put in the additional notes "prudent fiduciary guide," and I’ll email you a list of the "dos" and "don'ts" compiled from this legal case in a separate, simple PDF.

Fiduciaries must make a diligent effort to compare alternative service providers in the marketplace, seek the lowest level of costs for the services to be provided, and continuously monitor plan expenses to ensure that they remain reasonable under the circumstances. (Page 11)

If you’re a benefits leader, take a second to re-read this statement and acknowledge that the case states the responsibility of continuous monitoring several times throughout the document. In my experience, fiduciaries either don’t know this responsibility exists or don’t know how they can possibly comply with the high standard since in practice this does not seem to be the case.

Shameless plug: this is why we started TrueClaim. We can help your overworked benefits team meet the bar for continuous monitoring of your plan expenses.

Anyone who exercises any discretionary authority or discretionary control over the management of an employee-benefit plan, and anyone who exercises any authority or control respecting management or disposition of the assets of an employee-benefit plan, is a fiduciary of the plan…Any person who is a fiduciary with respect to a plan who breaches any of the responsibilities, obligations, or duties imposed upon fiduciaries by this subchapter shall be personally liable to make good to such plan any losses to the plan resulting from each such breach, and to restore to such plan any profits of such fiduciary which have been made through use of assets of the plan by the fiduciary, and shall be subject to such other equitable or remedial relief as the court may deem appropriate, including removal of such fiduciary. (Pages 10-12)

Many benefits leaders and executives are unprepared for the level of personal liability laid out in the lawsuit when it comes to controlling healthcare spending. In addition to the company (JnJ), the plan, and its benefits committee, specific individuals with fiduciary responsibilities are named defendants in the case (Executive Vice President and Chief Human Resource Officer; Vice President of Human Resources; etc.). The case cites the fiduciary responsibilities of the individuals in addition to the process and plans carried out by the committee and cites their personal liability as fiduciaries.

Traditional PBM Model (Pages 15-20)

This section is a crash-course on different techniques PBMs use to take money from self-insured employers. It should be required reading for anyone signing their company up for prescription benefits. My personal favorite is section 56, which covers how PBMs can recreate the effects of spread pricing but hide it behind owning their own pharmacies and driving customers to those pharmacies.

According to one report, an EBC (employee benefit consultant) managing an RFP process refused to allow a PBM to even enter a bid for a plan’s contract unless the PBM agreed to pay the EBC $6.50 per prescription. In an apparent attempt to hide the payment, the EBC asked the PBM to mail the payments quarterly to a PO box in another state. (Page 23)

Defendants Mismanaged The Plans’ Specialty-Drug Program (Pages 31-45)

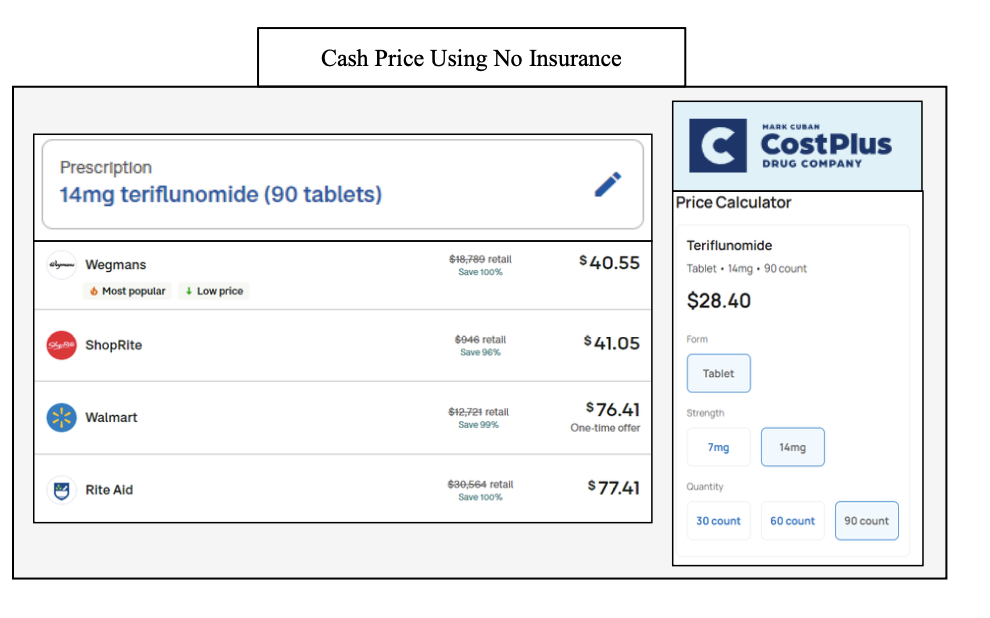

Now we dive deep into how mismanaged specific aspects of the drug plan were at JnJ. While the case argues an average 498% markup above cost on generic-specialty drugs, specific examples are given that compare cash cost from services like Mark Cuban CostPlus Drug Company (opens in a new tab) and GoodRx (opens in a new tab) that show much higher markups, including 12,403% on one drug (Temozolomide, a generic cancer drug).

This analysis is what TrueClaim does on an ongoing basis. For any self-insured employer reading this, if you provide TrueClaim with your claims history, we show you what you’re overpaying in many verticals, including this comparison to cash for drugs. You can use this analysis to negotiate with your PBM, argue with your executive team that you should switch to a pass-through PBM, or engage with us directly to navigate your members to lower-cost options.

In an effort to measure aggregate overcharges of generic-specialty drugs, Plaintiff requested the formulary used by her prescription- drug benefits plan, administered by Express Scripts. Plaintiff was informed that she was not allowed access to her formulary. Accordingly, a publicly available Express Scripts formulary was used. (Page 42)

The case states that the plaintiff requested and was denied access to the plan formulary. My take here is that forward thinking plans should be able to see the writing on the wall when it comes to price transparency and lean into sharing more information rather than less right now. If your contract with your PBM prevents you from sharing your formulary, then that seems like the obvious place to start your journey towards fiduciary responsibility.

A Prudent Decision-Making Process Would Have Prevented Defendants’ Fiduciary Breaches… (Pages 60-64)

In this section, we highlight the "good guys," and see many ways self-insured employers have saved money by owning their formulary and negotiating with PBMs. Most useful, we see several case studies where large, self-insured employers switched from traditional PBMs to pass-through PBMs and saved 30-40% on their overall pharmacy spend.

....[health plan navigated patient towards a new site for care]...When Plaintiff asked if the health plan had reviewed cost prior to disrupting her care and directing her to the cancer center, they declined to provide any evidence that the cancer center was lower-priced than her original treatment site, and on information and belief, it was not….Nevertheless, the plan denied her request, going so far as to tell Plaintiff that "saving money is not a reason to go out of network." (Page 66)

Wow, they said this out loud! Crazy! Any navigation effort on behalf of a plan needs to be able to back up their choices with reasoning on both the clinical and the cost savings side of things. It’s absurd that the cited case seems to provide neither and even goes so far as to tell a motivated plan member trying to save money “that’s not what we do here.”

Under 29 U.S.C. § 1132(c)(1), any plan administrator “who fails or refuses to comply with a request for any information which such administrator is required by [ERISA] to furnish to a participant or beneficiary ... within 30 days after such request may in the court’s discretion be personally liable to such participant or beneficiary in the amount of up to $100 a day from the date of such failure or refusal, and the court may in its discretion order such other relief as it deems proper.” By regulation, the penalty has been increased to $110 per day. (Page 72)

One of my favorite parts of the lawsuit highlights the plaintiff’s experience accessing plan documents. The plan documents reference more plan details provided on a company web page, but the member could not find or access the detailed document on this website. The member requested the documents be mailed, since they could not be accessed online, but received documents in the mail for a different plan than the one they utilized. While this experience highlights the importance of operational excellence in plan administration, it also gives a glimpse into the reality of patients navigating their healthcare - what stood out to me is how ordinary this experience feels. I think we can all relate to the annoying bureaucracy and incompetence encountered when trying to perform basic actions with your healthcare plan. It’s great to see this being called out and penalized!

How do I avoid becoming the next JnJ?

TrueClaim can help employers get an unbiased understanding of where they are overspending on healthcare. As part of our one-time, free claims analysis we provide the type of comparison laid out in this lawsuit for prescription costs for members under their PBM contract compared to industry-standard and cash-based prices for the same drugs. Usually, we see this pharmacy analysis in the top 3 verticals self-insured companies can focus to reduce costs.

This case is only the beginning. We will continue to see fiduciary breach cases, backed by the CAA legislation, hit self-insured employers. The cases will expand from pharmacy-based arguments to also include medical, examining employers’ contracts with Third Party Administrators and insurance companies. Prudent fiduciaries will act now in their own and their plan members' best interest to get control of their healthcare spending.

© Bobby Bayer.RSS